January 19, 2023

Editorial Disclaimer

This content is published for general information and editorial purposes only. It does not constitute financial, investment, or legal advice, nor should it be relied upon as such. Any mention of companies, platforms, or services does not imply endorsement or recommendation. We are not affiliated with, nor do we accept responsibility for, any third-party entities referenced. Financial markets and company circumstances can change rapidly. Readers should perform their own independent research and seek professional advice before making any financial or investment decisions.

As a business owner, you've got a lot on your plate. As a business owner, you're responsible for envisioning and implementing ideas and strategies to drive your company forward. You're also the marketer, spreading the word about your products or services. But there's one major responsibility that sometimes gets pushed aside, managing the finances.

Accurate bookkeeping serves as the foundation for any thriving business. Effective bookkeeping supplies vital information for making informed decisions, ensuring the long-term success of your company.

This article covers the fundamental aspects of bookkeeping that every entrepreneur should master.

The foundation of sound bookkeeping lies in meticulous record-keeping and transaction categorisation. It's alarming that 50% of small business owners feel they lack accounting knowledge, which can lead to costly mistakes. To avoid this pitfall, establish separate business and personal bank accounts for clarity in financial transactions and compliance.

Additionally, categorising expenses and revenue streams is crucial for identifying patterns and making informed business decisions. Whether you're tracking marketing costs, inventory expenses, or sales figures, consistent categorisation paints a vivid picture of your financial health.

Regularly update your books using accounting software or through the services of a professional bookkeeper, as recommended by experts. For instance, many organisations provides reliable bookkeeping services in places like San Francisco. If you need assistance, consider searching for bookkeeping services near me to find local professionals who can guide you through the process.

Selecting the right accounting method is crucial for aligning your financial tracking and reporting with your business objectives. The two main methods are cash and accrual accounting, each with its advantages and considerations.

Cash accounting is often the preferred choice for smaller businesses and service-based industries with straightforward operations. As the name suggests, transactions are recorded when cash is received or paid, providing real-time insights into your available cash flow. This method is simpler and easier to maintain, making it a suitable option for entrepreneurs who prioritise a clear understanding of their liquid assets.

When short-term business loans are part of your strategy, accurate tracking protects your cash flow.

On the other hand, accrual accounting offers a more comprehensive financial overview, making it the preferred method for larger businesses, product-based industries, and companies with complex operations or inventory management requirements.

Under this method, transactions are recorded when revenue is earned or expenses are incurred, regardless of the actual cash exchange. This approach provides a more accurate representation of your profitability and financial performance, enabling detailed analysis and projections.

While the accrual method may be more complex due to the consistent tracking of accounts receivable and payable, it offers a clearer picture of your business's financial health. Transitioning to accrual accounting can provide valuable insights for strategic decision-making as your business grows and operations become more intricate.

To help you make an informed decision, consider the following comparison between cash and accrual accounting methods:

| Aspect | Cash Accounting | Accrual Accounting |

|---|---|---|

| Basis of Recording | Transactions are recorded when cash is received or paid | Transactions are recorded when revenue is earned or expenses are incurred, regardless of cash exchange |

| Suitability | Best for small businesses, service-based industries, and businesses with straightforward operations | Preferred for larger businesses, product-based industries, and businesses with complex operations or inventory |

| Financial Insights | Provides a real-time view of available cash | Offers a comprehensive view of profitability and financial performance |

| Tax Implications | Taxes are paid on cash received | Taxes are paid on revenue earned, regardless of cash receipt |

| Complexity | Simpler and easier to maintain | More complex, requiring consistent tracking of accounts receivable and payable |

While cash accounting offers simplicity, accrual accounting provides a more accurate representation of your business's financial position, making it the preferred method for most growing businesses.

In today's busy business world, adopting technology is essential for efficient bookkeeping. Cloud-based accounting software streamlines the management of transactions, receipts, and financial reports.

Remarkably, 95% of accounting practices have embraced cloud-based software to some degree, and 63% report improved client services as a result. The role of technology in modern accounting tasks not only saves time but also reduces the potential for human error.

While bookkeeping involves the day-to-day recording of transactions, understanding financial statements is crucial for gaining a holistic view of your business's performance. Three key documents every entrepreneur should familiarise themselves with are:

Regularly reviewing and analysing these statements empowers you to make informed decisions about resource allocation, debt management, and growth opportunities for business development.

While entrepreneurs often strive for self-sufficiency, collaborating with professionals can be a game-changer in managing your finances effectively. Although only 14% of small business owners believe accountants could do more to reduce their taxes, involving a certified public accountant (CPA) or a bookkeeper can provide invaluable insights and ensure compliance.

Many businesses today also rely on outsourced bookkeeping services to handle day-to-day financial management while freeing up time to focus on growth. Treat these professionals as partners who can not only handle tax preparation and bookkeeping tasks but also offer strategic guidance on financial planning, tax optimisation, and process improvement. Maintain active involvement by reviewing reports and ensuring alignment with your business goals and objectives.

Bookkeeping is an ongoing process that requires regular review and improvement. While 21% of small and medium businesses (SMBs) review their books monthly and 18% quarterly, it's advisable to establish a consistent schedule that aligns with your transaction volume and business cycles, especially for businesses relying on bookkeeping in Melville, NY to maintain accurate financial records and stay compliant.

Periodic reviews allow you to identify discrepancies, monitor financial health, and course-correct as needed. Implement processes for consistency, ensuring proper checks and balances. Additionally, anticipate large expenses by budgeting at least quarterly to mitigate risks and maintain a solid financial footing.

As an entrepreneur, you must be prepared to navigate challenges and embrace growth opportunities. Recognise that seasonal changes and business cycles can impact profitability, and adapt your strategies accordingly.

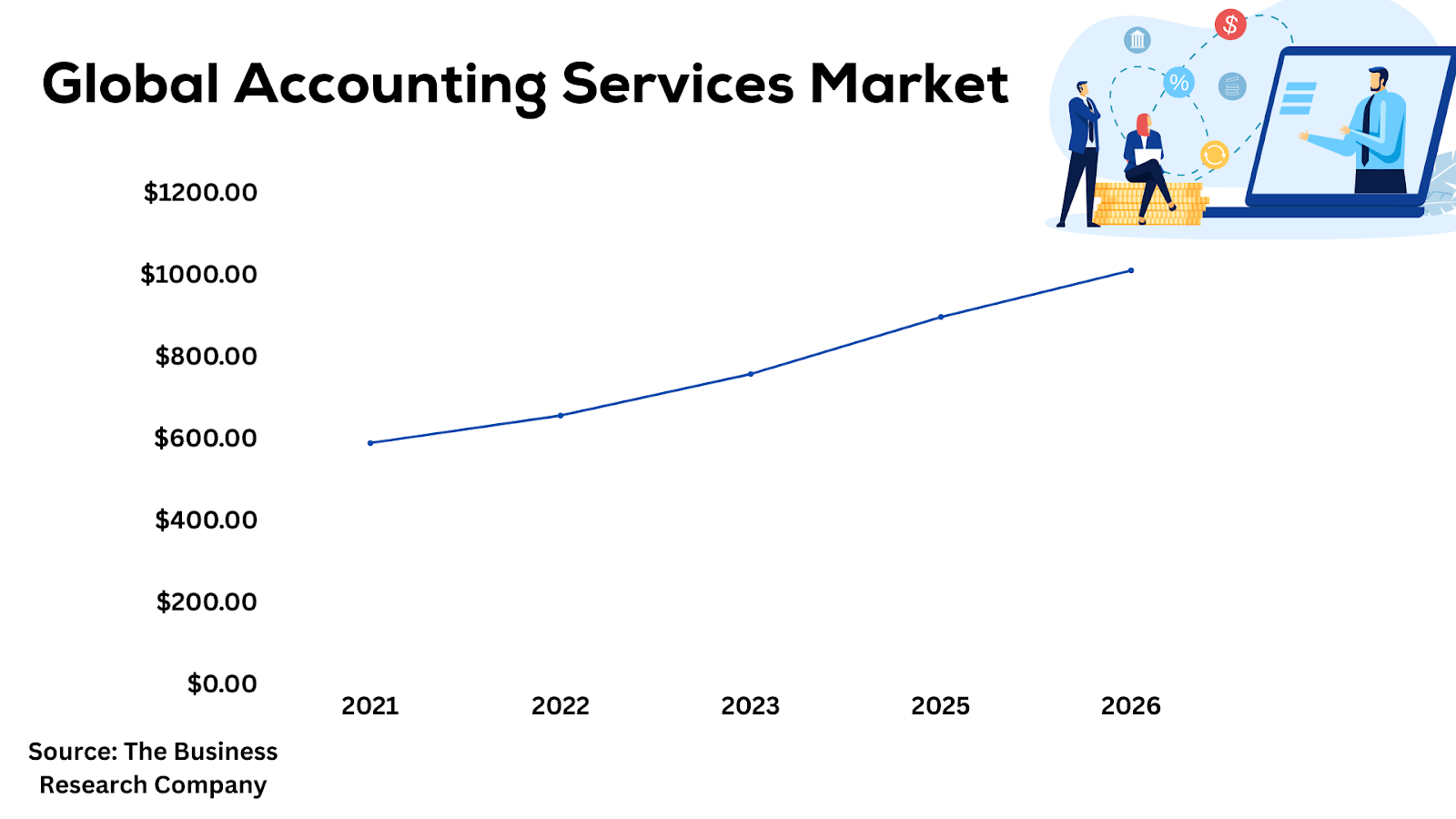

Allocate resources and build reserves to weather financial uncertainties, and continuously refine your bookkeeping habits to align with your growth goals. With the accounting services market expected to grow to $1,009.51 billion in 2026 at a rate of 11.4%, staying ahead of the curve is essential.

Effective bookkeeping is the foundation upon which successful businesses are built. By prioritising accurate record-keeping, choosing the right accounting method, embracing technology, understanding financial statements, collaborating with professionals, and regularly reviewing and improving your practices, you can guide the entrepreneurial journey with clarity and confidence.

Remember, bookkeeping is not just a compliance exercise but a strategic tool that empowers you to make informed decisions, identify growth opportunities, and steer your business toward long-term success.

Take the first step towards mastering bookkeeping by evaluating your current practices, exploring automation tools, and seeking professional guidance. Invest in your financial literacy today, and watch your business thrive.

The choice between cash and accrual accounting depends on factors like business size, industry, and reporting needs. As mentioned earlier, smaller businesses may prefer cash accounting for its simplicity, while accrual accounting offers a comprehensive financial overview better suited for growing businesses.

Ideally, you should update your records daily or weekly, depending on your transaction volume. Consistent updates ensure accurate tracking of your financial health and enable better decision-making, as recommended by experts.

The balance sheet, income statement, and cash flow statement each offer unique insights into your business's financial performance. Together, they provide a comprehensive understanding of profitability, cash flow, and overall financial health.